The last 14 months since the Cedigaz long-term-contracts database (1) was last updated has shown a continuation of the wave of renegotiations that has gained momentum since 2010, recently culminating with the announcement by ENI of its agreement with Gazprom. The deal, which reduces both the price and take-or-pay obligation of contracted gas, has been hailed by the gas community has signaling a move away from oil-indexation by the Russian gas giant. Based on ENI’s declarations some analysts contend that the gas is now 100% hub indexed. According to Argus Media, the actual arrangement is more subtle, the pricing formula would still be oil-based but would include a price corridor based on TTF prices.

Analysis - Page 10

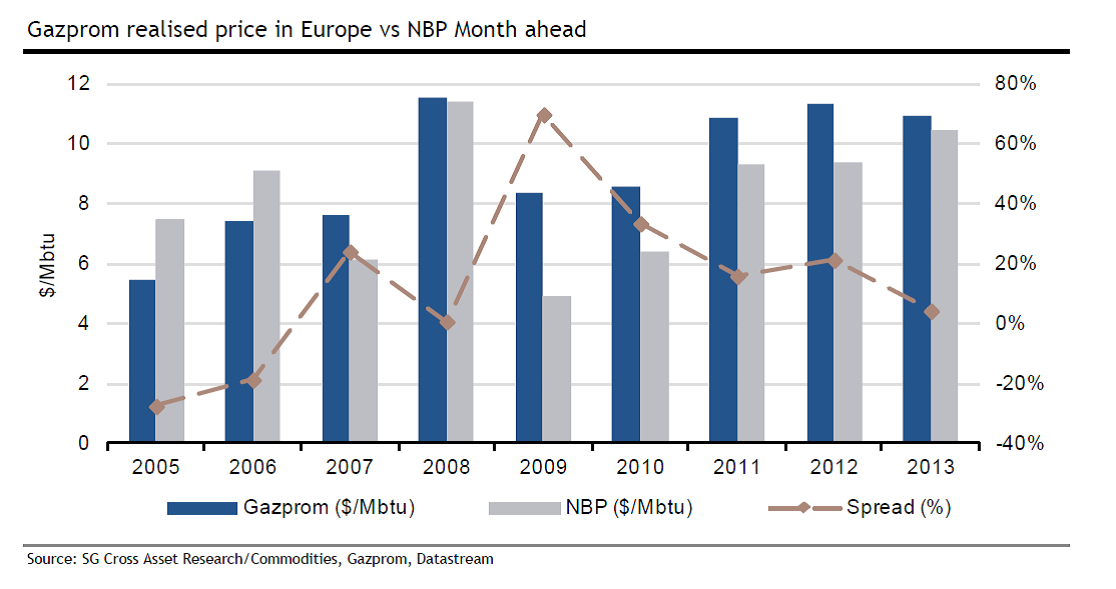

Putting a price on gas or Putin’s gas price?

By avoiding pushing too much volume, Gazprom/Russia and Statoil/Norway not only avoided a price war in 2011-2013 but managed to reset spot prices at a level that is acceptable to them.

Higher prices were leading to permanent demand destruction. Russia is not willing to boost European gas demand for power generation at a price that it considers too low. As even with no growth in demand, Gazprom’s volumes are rising to mitigate the decline in European gas production.

So why has Gazprom provided additional volumes to Europe at the expense of prices, that went down by 40% since end-2013? Higher prices were also leading to the development of alternative supply. With the Final Investment Decision (FID) in December 2013 for Shah Deniz 2 in Azerbaijan and a long list of potential LNG projects in North America, Russia could see the threat of new suppliers/competitors entering the European market after 2020e.